Interview with Trevor Hill of FATHOM by The Water Network

Published by Water Network Research, Official research team of The Water Network in Business

In 2009, Global Water launched FATHOM (TM), a technology enabled software-as-a-service platform designed to provide state of the art back-office services to municipal water utilities. The Water Network team has a pleasure to talk to Trevor Hill - co-founder of both Global Water and FATHOM. Prior to that, he co-founded Algonquin Water Resources of America in 2003, a division of the Algonquin Power Income Fund, of which he served as Director of Operations from 2000 to 2003.

Q1 - Would you like to tell our members a little about your background? It would be lovely to find out how a naval officer became a water expert.

My passion for water technology does stem from my time in the Canadian Navy, where I worked on changing the technology we used to produce water while at sea. Seeing firsthand the difficulties of producing fresh water, especially as we began operating in hotter, more arid regions, inspired me to continue working in the water sector. During my time deployed to the Middle East, it became clear to me that water production and access to water would become a major global issue in the future. As such, I began formulating the thesis that water scarcity, and how we manage water would be a defining opportunity.

My passion for water technology does stem from my time in the Canadian Navy, where I worked on changing the technology we used to produce water while at sea. Seeing firsthand the difficulties of producing fresh water, especially as we began operating in hotter, more arid regions, inspired me to continue working in the water sector. During my time deployed to the Middle East, it became clear to me that water production and access to water would become a major global issue in the future. As such, I began formulating the thesis that water scarcity, and how we manage water would be a defining opportunity.

After retiring from the Navy, one of my Navy colleagues, Graham Symmonds, and I began a design-build engineering company focused on creating high quality recycled water to supplant potable water use. Most importantly, I recognized that the water industry – conservative by nature – needed business models that allowed for the adoption of technology and new processes while addressing and transferring risk away from the client. Ultimately what I decided that we would not be in the business of selling technology, but be in the business of solving seemingly intractable water problems, with technology, as a service.

Q2 - Why did you decide to start a water utility? And what is your experience with owning one?

As I mentioned, we wanted to be in the business of solving water scarcity. You can’t do that with technology alone. To achieve our goal of maximizing the efficient use of water we needed to have an impact not only in technology, but the operational management of water resources as well. That meant getting embedded with the utility – and what better way to do that than to own the utility itself?

We evaluated a number of regions and settled on Arizona as being at the intersection of water scarcity, population and demand growth and regulatory support for water reuse.

In 2001, we partnered with Algonquin Power Income Fund, and began acquiring utilities throughout Arizona and Texas. Through our partnership with Algonquin, we acquired 12 utilities. The partnership with Algonquin was—and still is—very successful. But we still wanted to do more.

In 2003, Graham and I, along with another Partner, Leo Commandeur, left Algonquin and formed Global Water Resources (Global Water), an aggregator of regulated utilities in the southwestern United States. This gave us the opportunity to get into the greenfield development of utilities, and impress the necessary physical infrastructure into the utility to maximize water efficiency. This meant recycled water mains in the street, advanced metering infrastructure, and most importantly, significantly improved back office and management systems. Through Global Water Resources, we were able to totally reimagine the water supply and management system—and thus defined The Smart Grid for Water.

Q3 - Could you name some novel technologies you adopted in your company that others were skeptical about? What impact did it have on your business?

As former naval officers, Graham and I never feared new technology. That’s partly why we started Global Water, because we could influence the technology that goes into water management and we could do it the best way we knew how. We pioneered the concept of the “fit-for-purpose water” in Arizona. That concept – using the right quality of water for the right use – is now standard in the state. Addressing the wide-scale adoption of recycled water was a decade in the making. Notably, we were an early and avid adopter of Advanced Metering Infrastructure (AMI) technology. Finally, I think we recognized early that there was value in the data of a water utility, but only if that data was correct and available to all, including our customers.

By integrating technology into our utilities, we achieved fantastic results. Through the application of basic technology, our utilities were operating with 46% less power, 65% less labor, 90% lower maintenance and repair costs than our peer group average—and bad debt decreased from roughly 10% to just 0.3%.

By using analytics to support collection activities and automated calls to customers at risk of disconnection for non-payment, we reduced our disconnections 90% and improved our customer satisfaction ratings significantly. Also, with visibility to real time, actual demands, we were able to reduce our distribution pressure overnight, which resulted in reduced water loss, fewer pipeline breaks and cut our electricity bill all at the same time. By putting water usage data in the hands of our customers, we achieved one of the lowest per capita water demands in our state.

Q4 - Do you think that utilities are slow when it comes to adopting new technologies? Which Utility you think is up-to-date with the existing technologies?

By nature, utilities are reluctant to adopt new technologies and capitalize on the first-mover advantage. As agents of public health, the water utility mandate is a simple one – provide safe reliable drinking water to our customers.

We also have to remember that water utilities are small. The EPA notes that there are more than 56,000 community water systems in the U.S. And the vast majority of those are small – 99.5 percent of them serving less than 50,000 people. This means that they lack the resources, skill and expertise to capitalize on technological opportunities.

So water utilities are generally small, cash strapped and risk averse because they are charged with the responsibility of keeping our water safe. They don’t have the time to commercialize technologies. Many great technologies die on the vine because they don’t recognize this fact.

In many ways water utilities want new technology, but technology companies are not providing the right business model and risk transfer to them.

Q5 - Would you like to share your thoughts on “Importance of big data and better information” for water utilities?

The water utility business is changing rapidly. Faced with the challenges of managing water resource scarcity in the face of growth and climate variability, managing financial survival, and responding to the information demands of technology-savvy consumers, utilities are discovering the need for, and power of, integrated data systems. Water utilities in the future will use faster access to better information to make better decisions and employ rapid dissemination of that information to consumers and other stakeholders.

These changes are being driven largely by increasingly limited water availability and the high costs of developing alternative supplies. Water utilities are now charged with blazing a path to sustainability through efficiencies for the utility and the consumer. As Dr. Peter Gleick of the Pacific Institute recently noted, the key to improving water efficiency is “understanding where, when, and why we use water.” Unfortunately, data of this granularity has been hard to come by in the water industry. In most utilities, data is a sparse commodity or is collected in such disparate platforms that interrelationships are missed or remain hidden.

The development of the smart grid for water is changing this paradigm by increasing the availability of data and information. The smart grid for water can tell us not only how much water is used, but where and when. The smart grid for water represents a significant shift from a data-poor, hardware-centric, asset-driven nineteenth-century model to a data-rich, information-centric environment that is 100 percent accurate and contextualized in space and time. This new approach has created the geotemporal data model, providing the where, when, and how necessary to understand water use, understand where opportunities for efficiencies exist, and engage the consumer in conservation.

Utilities around the world are therefore grappling with a fundamental shift in operational philosophy. We think of this as a shift from asset-centricity to meter- or customer-centricity. Not only must utility operators consider the customer impacts of the rising costs of water on their customers, but in fact provide those customers with the tools to understand and manage their own behavior. Regulators around the world are incentivizing water utilities to further engage their customers in these ways while demanding customer conservation and better operating efficiencies from the utilities themselves.

For our water utilities, focusing on collecting, aggregating, and analyzing this data to convert it into real-time information will be critical. The twenty-first-century water manager needs to manage the flow of data and information as equally well as the flow of water. Our future depends on it.

Q6 - Let us talk about FATHOM – what exactly is FATHOM? And how helpful it is to companies?

Q6 - Let us talk about FATHOM – what exactly is FATHOM? And how helpful it is to companies?

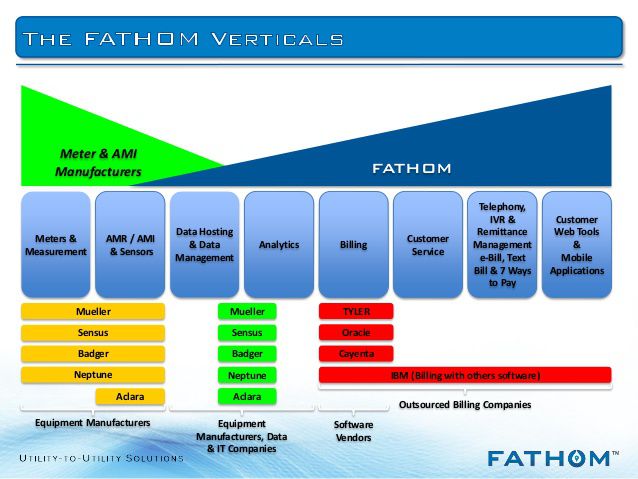

FATHOM is the largest software-as-a-service (SaaS) provider of geospatial time synchronized water IoT platform designed to redefine the vertical between the meter and the customer. We have partnered with over 50 technology providers and utility partners to leverage this platform to create an ecosystem of solutions that have been proven in operation and integrated to simplify the adoption of technology—creating the revenue utilities need to solve their challenges.

Having been developed by a water utility, FATHOM is specifically designed and architected for the unique needs of our industry. FATHOM is an end-to-end solution that can be adopted either as a whole or incrementally as needed, with each component designed to increase efficiencies and revenue and decrease operational costs.

For our complete Smart Grid for Water solution, we provide everything between the meter and customer. New meters, radio technology, AMI, customer information system, remittance management, customer care and web and mobile tools for customers. This solution also includes equipment installation and software implementation and configuration. We also provide municipal rate financing and operational guarantees for the equipment. For most of our clients they received our entire offering for less than they were spending already spending on maintaining their antiquated systems. With our repeatable processes and risk transfer mechanisms, utilities can adopt the latest technology without the fear of a failed implementation.

For some utilities, a full system change-out is not feasible, so we also offer an incremental adoption pathway. This path surfaces the data value propositions even faster and provides a way to allow utilities to experience the benefits of data without having to change every meter. With FATHOM Prime, we have created a pathway for the incremental adoption of AMI and the gateway to a smarter water utility.

Q7 - Can FATHOM work with multiple data systems like a manual or automatic meter reading, etc.?

Absolutely.

Historically, the water sector has been slow to adopt AMI because the value propositions were not readily realized with the antiquated data systems used in utilities. This means that most of our utilities continue to rely on manual and monthly AMR reads. We built FATHOM’s meter data management platform to handle this spectrum of conditions, while maximizing the value propositions associated with the available data.

Most importantly, we recognized that the need for data is increasing exponentially. As a result, we designed FATHOM to be the landing point for the water industry’s Internet of Things. So not only can we concurrently utilize all of the data from manual, automatic meter reading (AMR) such as drive by systems and Advanced Metering Infrastructure (AMI) fixed-network systems regardless of manufacturer, but we also take advantage data streams from inside utilities like distributed sensors in the water system, SCADA, asset management systems, and laboratory information systems, to geospatial data such as tax parcels, population demographics and precipitation. In fact, there isn’t a type of data FATHOM can’t utilize.

Q8 - Can a water company develop its own technology like FATHOM? Is it cost-effective?

In theory, a water utility could attempt to recreate the FATHOM platform for themselves, although it would not be cost-effective.

We have invested tens of millions of dollars into developing and refining the FATHOM platform and we will continue to do so to ensure that the platform continues to provide value to water utilities. We’ve also invested significant time and resources in developing partnerships with numerous technology providers and understand and integrate them into the platform.

To create a similar product would require a similar investment by any utility. Alternatively, we would suggest that rather than build it themselves, simply build upon the foundation that FATHOM has created with our platform as the Water Internet of Things. We are a water platform built by a water utility for water utilities and we believe that there is strength in numbers. Everyone is invited. FATHOM already hosts more data than any single utility in our sector, and we encourage other utilities to join the revolution and be part of the solution. Together we can change the water utility paradigm.

Q9 - How do you convince utilities to adopt FATHOM in the era of declining revenue for these companies?

Declining revenue is a real issue for water utilities. Thirty percent of utilities are seeing year over year revenue shortfalls as a result of voluntary and mandated conservation. The alchemy of FATHOM is that we have found significant revenue for our utilities in their own data. We have seen revenue increases of 5 to 15 percent simply as a result of deploying FATHOM’s data tools. As such, FATHOM is not a cost center, but a revenue center for utilities. In addition, we can demonstrate that FATHOM can perform functions like billing and customer service at a cost lower than the utility spends today.

Further, FATHOM utilities have access to tools that historically have only been available to the largest utilities.

FATHOM is an end-to-end solution that can be adopted either as a whole or incrementally as needed, with each component designed to increase efficiencies and revenue and decrease operational costs. So they get better tools, improved revenue, reduced costs, and better customer engagement – all in an easy software as a service business model.

In fact, many utilities find that FATHOM actually pays for itself.

With nearly 4 million meters on our platform across more than 140 water system, FATHOM is a risk free way to bring economies of scale to utilities with proven results of increased revenue, decreased costs and delighted customers.

Q10 - Are you collaborating with some other technology holders to make FATHOM better?

Definitely. We believe that only by uniting our water industry—both utilities and technology providers alike—on a common platform will we be able to achieve the scale necessary to ensure the long term success of the water industry.

Water is naturally heavy and extremely expensive to move, which has resulted in the creation of roughly 56,000 water systems in the United States alone. The vast majority of these systems are extremely small, having less than 1,000 connections on average. In short, our industry is fragmented.

This fragmentation makes it difficult for utilities to implement and adopt technology. These utilities are often budget and resource constrained so even if they can get themselves comfortable with the often significant risk involved in deploying new technology traditionally, they often can’t afford to pursue it. And too often, revolutionary technologies for the water industry end up dying on the vine because they cannot get wide adoption of their technologies.

Our platform is designed to bring this unity to our industry—from our data integration layer and long-term partnerships and integration agreements with several meter and device manufacturers.

In addition, we are launching the FATHOM Store, our online water utility marketplace. With the FATHOM Store, utilities can try and buy vetted third-party technologies that have been pre-integrated with the FATHOM platform to reduce both risk and resources required to implement these technologies. Technology companies will be able to market and sell their applications directly to the hard-to-reach water utilities.

We believe that there is strength in numbers.

Q11 - What future plans do you have for FATHOM? Are you looking to enter the global market in the future?

While FATHOM was born out of a U.S. water utility, the value that FATHOM can provide through our Smart Grid for Water resonates worldwide. Discussions about water safety, water scarcity and vulnerability are captivating audiences all over the world, including Southeast Asia, Italy, Singapore and Australia to name a few. As such, I believe FATHOM will expand to three or four countries over the next two years.

The future for water utilities around the world is technology and big data. They are the vehicles through which the next generation of risk management for utilities will be managed—from water scarcity and climate change, aging infrastructure, technological innovations and increasing customer expectations.

Tags

Category: Business

- Water

- IT

- Geospatial Information Systems

- IT

- Software & Services

- Water Software

- Smart Metering (AMI)